The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Bulls finally running?

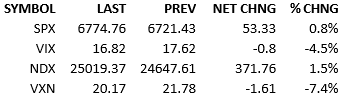

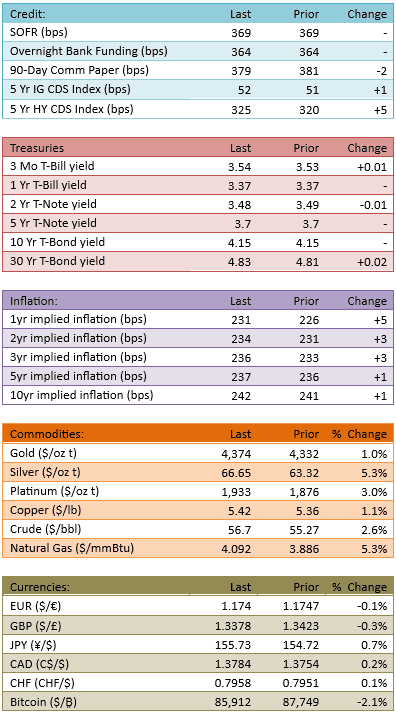

Overnight futures were bid slightly, a common occurrence of late. CPI data released at 8:30 AM and it was cooler than expected. Two months of data released and there were/are some questions when one looks under the hood but the market was pleased with the cooler inflation numbers and equity futures kicked things up a notch. The S&P opened about +50 and wandered around from +40 to +95 over the day. Yields came in across the curve, a welcome change for both equity and bond markets. Fed Funds futures now price a 25-bip cut in January with 27% probability, a slight increase from yesterday.

While many on the Street are suspicious of the CPI data, the consensus is that the adjustments and oddities are not political but simply best-efforts guestimates because the shutdown resulted in various data gaps. It’s a very inside baseball conversation that’s ongoing out there…and not too relevant to the larger market reactions.

The big picture concerning inflation is that it is *not* climbing. That allows the Fed to remain dovish and that allows the inflation fears in the bond market to settle down. The overall result is very helpful for risk-on investing. The stock market responded accordingly although it didn’t rally very much today, all things considered.

The Fed’s actions and path is always a balance of their dual mandate but they have publicly stated that they favor rate accommodation on behalf of labor market risks since September. Inflation data at the time was 50/50, in terms of whether it was declining or not. The Fed chose to risk inflation for the sake of helping labor, and the market agreed with the trade-off.

But over the months, the market started to worry that inflation risk was increasing. The Fed remained confident. There was a market concern that the Fed was committed to easing, with inflation consequences pending as a considered cost. Today, a different conclusion can be given weight.

The Fed can continue to ease and inflation can stay, or fall.

This is a Goldilocks possibility. The market hasn’t latched on to yet but it is warming up to it. If this is how things play out, the next few months will be very good for risk-on players.

Today’s modest gain is the first step of the market pricing in Goldilocks. We’ll see if data and sentiment can deliver more price-steps. If we get those, new highs will print before year-end.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.