The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Off and running.

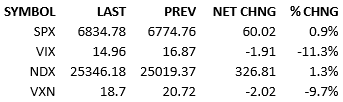

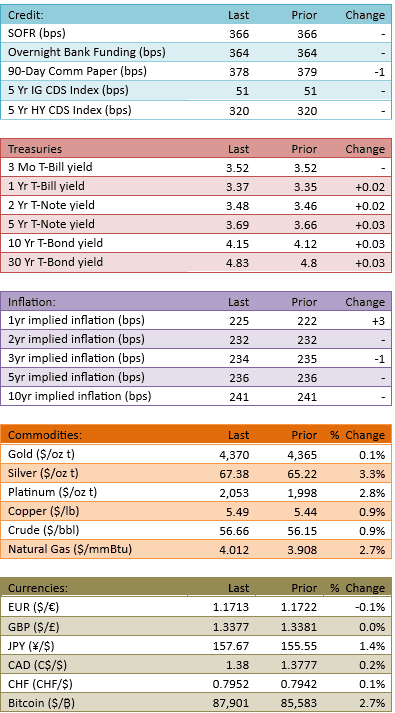

Futures rallied small at 2 AM and the S&P 500 index opened about +25. The index immediately climbed further, settling in around +45 before lunch and climbing slightly further thereafter. Treasuries weren’t as kind to their holders as yields climbed across the curve again. News and data didn’t push prices noticeably today so it appears that the sentiment of the crowd was the factor of note.

If late-December buying was destined to show up, we might have heard the starter’s pistol yesterday. Today looks very much like continuation. If the weekend is quiet, next week could be very nice for the longs. The usual dip-buyers were surprisingly patient over the last two weeks but with two strong up-sessions in the books, it looks like the most recent drop in stocks is over and the local bottom is printed.

The usual playbook applies and we *should* see players pile in until we get new highs (9620). That’s not too far away so there could be a pretty quick scramble to chase offers and get in under the previous highs. As long as headlines cooperate, we will make new highs before Christmas.

When it came to today’s rally, one would have expected the Mag 7 stocks to lead the way but they didn’t trade together. Nvidia led and the rest were mixed. Oracle also had a huge day as the market returned to the AI complex. Those stocks are the quintessential dip-buyer opportunities, having been punished more than the rest over the last two weeks.

The S&P is down small for the month, up 16% for the year. If longs want to put a cherry on top, it’s now or never.

See you Monday, have a great weekend.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.