The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Fizzle

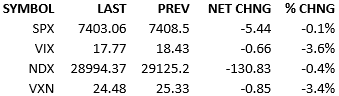

Investor moods slid backwards some today. Yields picked up a bit. Crude climbed some on the front-end. US/Iran negotiations continued to go nowhere. The risk-off reaction of Friday continues to a lesser degree today. Headlines were fairly tame so other than a lack of progress between the US and Iran, today’s moves seem to be driven my current investor sentiment rather than fresh catalysts.

Perhaps this is just the start of a digestion of the large recent gains of the market. We’ve known that the rally from late March would end at some point and it looks like that point was Thursday. Whether we digest the enormous gains in a sideways or downward path is anyone’s guess but it make just be the nature of markets for us to experience a bit of a cooling of sentiment without clear causes in the news.

That said, bulls are always on the lookout for a fresh upside impulse and Nvidia’s earnings announcement is their go-to event. Nvidia announces after the close Wednesday. Everyone expects them to beat the published estimates. Considering how almost every shareholder also expects significant boosts to guidance, it will be tough for NVDA to beat all the unpublished expectations. We shall see soon enough. NVDA is up 11% month-to-date, with much of that reflecting optimism concerning their coming announcements.

Whether NVDA justifies its recent climb or not, it will certainly be a moment for the entire market.

It could trigger a whole new rally higher or it could justify the digestion period we’ve just begun.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.