The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

The party continues

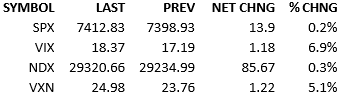

Despite the all-too-familiar problems with the US/Iran negotiations, markets continued their trend. The domestic headlines were pedestrian and investors mostly continued the moves from last week. S&P futures traded slightly lower overnight and in early trading but US investors pushed prices up during regular trading hours. The index opened down about 10 points and quickly lifted to spend the day in the +10 to +30 point range, finishing up small at the close. Crude and Treasuries reacted to the US/Iran difficulties as per usual. Crude climbed across the curve, with the biggest gains in the front. Yields climbed across the curve, flattening slightly from 2 years to 30.

US equities seem to be immune to negative US/Iran headlines now. Crude and bonds still react to each day’s developments and they appear to be fairly sensitive to even minor news. Crude’s sensitivity makes all the sense in the world. Why Treasuries are so sensitive is less clear. Why equities are ignoring US/Iran things is also less clear.

It’s certainly a weird situation. It’s not unusual to see stocks and bonds react differently to situations. Typically, it’s interpretation of Fed communications or macroeconomic data. And over time, the two markets eventually converge somewhere and pretty much return to trading in agreement thereafter.

This circumstance is quite different because we’re dealing with political news and outcomes. It’s also different in that the most influential mechanism upon capital comes from crude prices, which is obvious to all and subject to almost no interpretation. Why are Treasuries trading with crude while stocks trade indifferently to it?

I have no good answer. That said, perhaps having an answer isn’t germane. The reactions are observed and that’s more important than understanding why.

Baring horrific US/Iran headlines, expect stocks to continue to party. They may be overbought but they’re still climbing. When it ends, it probably won’t end ugly. It probably just fizzles out. The dip-buyers almost certainly will catch the tape.

And here’s the kicker. *If* a US/Iran deal gets made, Treasuries are going to jump, crude is going to drop, and yes, stocks are going to extend their rally.

Stocks are considered the risky asset class but lately they’ve been counterintuitively bulletproof.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.