The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Ceasefire extension?

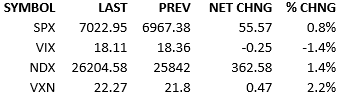

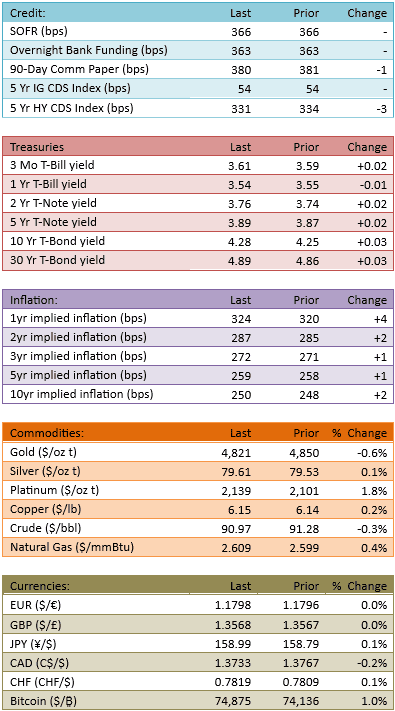

The US/Iran ceasefire continues and while the Strait of Hormuz lacks shipping traffic, markets are taking comfort in the fact that neither side is attacking the other. The Israel/Hezbollah fighting continues, which complicates the US/Iran negotiations, but markets aren’t concerned with the fighting in Lebanon at the moment. Anyway, a two-week extension of the US/Iran ceasefire is being bounced around and investors are pleased by the idea. The S&P opened about +10 today and rallied further over the course of the day, printing new all-time highs in the afternoon. While equities climbed, bonds fell slightly. Yields climbed 1-3bips across the curve. Crude increased small across its curve as well.

The bull market continues as long as the US/Iran situation proceeds smoothly. The logjam in the Strait remains problematic for global trade and price normalization but markets are not concerned with that yet. Markets are assuming that as the US/Iran negotiations progress *without a resumption of violence,* the shipping will resume soon enough and the resulting economic frictions will ebb.

At some point, the market will need to actually see shipping normalize in the Strait but we’re not at that point yet. Nobody knows when the market’s patience will wear out regarding that either, so there is a ticking clock at play. However the situation is not as tense as the prior weeks, so that is nice. We’re just not out of the woods.

Earnings season began and so far the results are good. Most stocks are beating the Street, which is typical. We’ve only seen a handful of results so extrapolation makes no sense but the *mood* surrounding the season has improved. It doesn’t seem like markets are expecting fireworks and massive rallies due to earnings… but the worry about disappointments seems off the table. There was prior concern about how the Middle East conflict could hurt corporate results. So far, that concern is misplaced and investors are breathing a little easier.

16 S&P 500 constituents report over the remainder of the week and then the floodgates open. We’ll have to analyze that data but the market’s attitude is good.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.