The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Not promising.

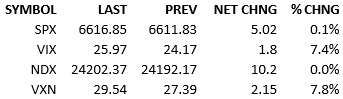

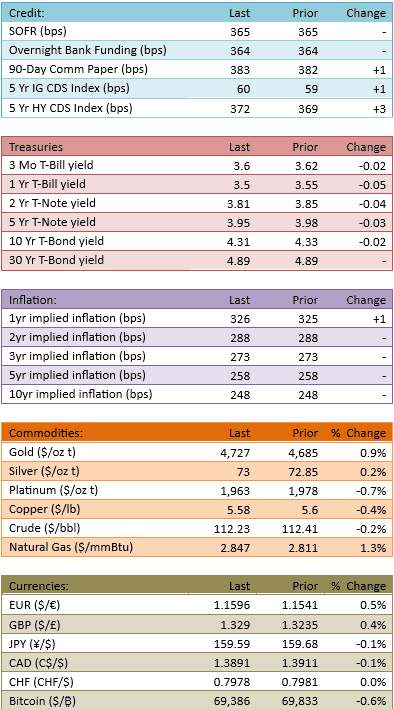

Despite the 8 PM deadline, there’s been no meaningful progress on the US/Iran situation. Markets, which yesterday assumed things would proceed in some acceptable way, started throwing in the towel today. Premarket futures bounced from down 30 to up 10 and the S&P 500 opened about down 20. Regular hours trading took the index further lower in the morning, rebounding significantly by early afternoon, slipping again mid-afternoon, and finally popping up late, on headlines suggesting deadline extensions. Capital flow was light again today, 71%. The yield curve steepened a bit, essentially undoing yesterday’s move.

We are almost at the moment of truth. Will a last-minute miracle of diplomacy result? If not, how furious will the military actions get?

Markets are now waiting for actual events to unfold. The discounting and handicapping are done. Tonight, in Asia, in tomorrow’s waking hours, in Europe, and come mid-morning, in the US, markets will be repricing. We will reprice based on the results of events. We will also begin discounting and handicapping the new potential paths and outcomes that result from whatever actually happens this evening.

See you tomorrow.

-Mike

Visdom Market Commentary

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.