The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

It’s dicey.

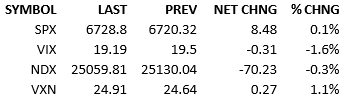

Risk-off momentum gathered steam in the premarket as S&P futures went south around 6 AM. The index opened down about 30 points. Asian markets had already closed down about 1% and Europe was down about 0.8% at that time. Headlines were lacking any smoking guns. Investors were simply worried this morning and the worry built on itself. The index bottomed around noon, with the S&P down about 90 points at the time. Like so many dips this year, it was bought. Damage was slowly repaired all afternoon when the buyers made a real run higher at 2:30 PM. The index got to unch’d for a second around 3 PM and went slightly positive in the final minutes.

Nervousness is the atmosphere but the urge to capitalize on dips remains strong. The rally in the afternoon appears to be rooted in an overture by the Democrats to the Republicans to reopen the government. This was an unexpected positive. The tape pulled back some when news broke that the Republicans would likely not accept the deal that the Democrats put on the table. That’s a negative for sure. But here’s the key, there’s *movement.* The two sides are finally talking turkey. This is a sign that *something* will happen and that the stalemate of the last 30-some days will end.

I don’t know how long this bartering-phase may go on. It may last too long of coure. Markets may get more scared… but the frozen positions of the powers in D.C. appear to be thawing. I think the writing is on the wall, for anyone brave enough to speculate. Buy the dips now, hold on to some capital for a further scare in the coming weeks, but be ready for a heck of a rally once the deal is announced and the government re-opens.

The reopening of the government is a necessary, but not sufficient, condition for the bull to continue to run for the rest of the year though.

For recent/near-term buys to generate gains by the year-end, we will need to see *data* that confirms that we are not declining into recession. That data needs to be collected and published by the government. So an eventual deal in D.C. will spark a strong and quick rally but the continuation of the bull will require economic verification.

That’s not a slam dunk case but it’s a descent probability. Let’s see if Congress can get the first part done. For the first time in a long time, it’s plausible.

Have a great weekend, see you Monday.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.