The opinions expressed below are my own and do not necessarily represent those of Visdom Investment Group, LLC.

Note: I’ll be out tomorrow, so next recap will be Monday.

Neglect?

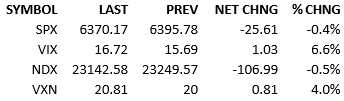

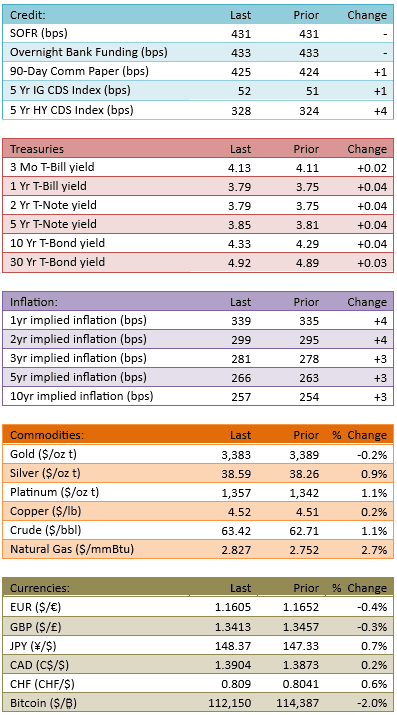

Overnight and early morning futures trading were flat but they began to sag around 5 AM. The macroeconomic data releases painted the usual pictures. The US economy appears to be moving along just fine. Yields across the Treasury curve rose slightly and the hyper confidence of a rate cut from the Fed is now just high confidence. The current probability of a Fed cut on September 17 is 72%. About a week ago that was 100%. News wasn’t interesting and so we can’t point to headlines to explain the price action. The S&P opened down about 25 points, tried to get to flat, rolled over, and treaded water around down 25 for the bulk of the afternoon. Capital flow was *very* light today, printing 81%.

Today was quiet and boring. The fact that the bears won the session, and are on a 5-session down streak, are what most are discussing. That’s kinda sorta interesting. Sure. It’s been a bull’s world so a bear’s week is worth chatting about.

I find the lack of volume compelling. This summer has been seasonally active. We haven’t had the typical summer doldrums. Today certainly qualifies as a slow summer session.

Whether it took the whole summer for investors to finally take their vacations or whether there’s some other reason, I’m not sure. I am struck by the fact that on a session when the capital flow finally lightened up, the tape sagged. Twenty-ish points aren’t significant but I don’t think this is a coincidence either.

We all know that retail has been relentlessly buying the market over the year. The pros have essentially been doing the same. Tomorrow we hear from Fed Chairman Powell at the Jackson Hole conference. Maybe everyone is pushing pause on their plans until they hear what he has to say?

Maybe, without the usual flow of buyers, the tape slipped lower?

It’s weak gruel but it’s the only gruel I’ve got. I think the usual buyers were absent today, because they’ve finally taken a summer break or they’re waiting on Powell. His comments publish tomorrow at 10 AM, so we will find out then.

If I’m right, and Powell says anything non-hawkish, we’re going to rally into the weekend.

If I’m right, but Powell says some hawkish things that the market is worried about today, we are going to lose a percent or two on Friday.

If I’m wrong, that means that the market wasn’t waiting on Powell, so who knows what will inspire it.

I’m betting on a Powell-inspired rally.

I’m off tomorrow, see you Monday, have a great weekend.

-Mike

IMPORTANT INFORMATION

This is general educational information and market commentary and is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

All market and economic data herein is as of the date hereof and sourced from Bloomberg unless otherwise stated. The information is subject to change without notice and we have no obligation to update you.

This general market commentary is intended for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The views and opinions expressed constitute the author(s) judgment based on current market conditions, are subject to change without notice, and may differ from those expressed by other employees of Visdom Investment Group LLC ("Visdom") and Visdom. Past performance and any forward-looking statements are not guarantees of future results. It is not possible to invest directly in an index.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation; however, we do not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. Any securities referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by Visdom or by the author(s) in this context. The information presented is not intended to be making value judgments on the preferred outcome of any government decision. This information does not constitute Visdom research, nor should it be considered a recommendation of a particular investment strategy or an offer or solicitation for the purchase or sale of any financial instrument. Investing involves market risk, including the possible loss of principal. You should speak to your financial advisor before making any investment decisions. Visdom and its affiliates do not provide legal, tax or account advice so you should seek professional guidance if you have questions.